Hormuz closure sparks 11% surge in EU natural gas futures

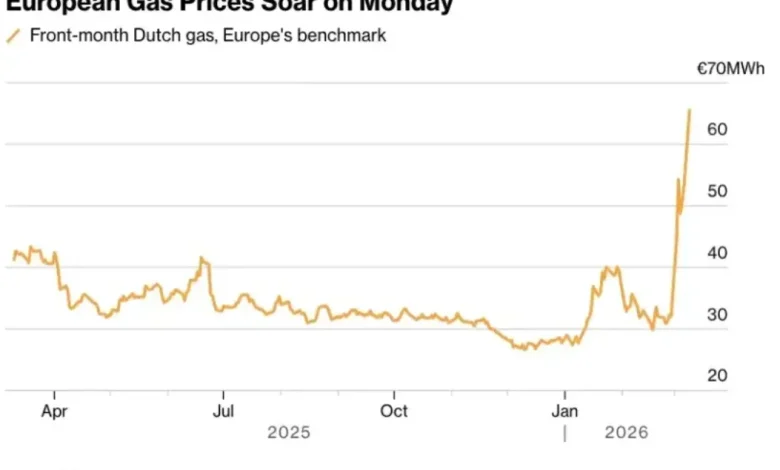

Hormuz drama continues to dominate global financial exchanges this morning as European natural gas futures aggressively skyrocketed by up to 11%. Reaching a shocking €43 per MWh at the start of today’s trading session, the staggering surge directly follows Iran’s abrupt announcement regarding the re-closure of the critical maritime chokepoint. Market participants, who had tentatively breathed a sigh of relief following a brief, chaotic opening of the waterway over the weekend, are now grappling with an incredibly volatile and hostile macroeconomic reality. As cargo vessels hastily attempted to exit the heavily contested waters during a momentary easing of tensions, international supply chains were violently disrupted once again when Tehran shut down transit capabilities. This unprecedented move represents a direct retaliation against the intensifying, ongoing U.S. blockade. The swift geopolitical reversal totally erased Friday’s late-session price drops, transforming energy markets into an erratic pendulum. The sudden price shock leaves European nations frantically bracing for further economic instability, acutely feeling the severe heat on their domestic gas indices just as the continent struggles to manage the lasting energy fallout stemming from the protracted war in Ukraine.

The Weekend Reprieve and Sudden Closure

During a bizarre and fleeting window over the past weekend, a series of mixed signals emanated from the Iranian Revolutionary Guard Corps, temporarily suggesting a de-escalation in the vital shipping lane. Several heavily laden vessels, including a rogue supertanker defying blockade orders, managed to execute daring dashes out of the Persian Gulf. International commodity traders largely interpreted this momentary lapse in absolute closure as a potential thaw in the standoff, prompting a sharp, yet incredibly brief, sell-off in natural gas and oil futures on Friday afternoon. However, the optimism proved profoundly premature. By late Sunday night, Iranian authorities officially reversed course, declaring the strategic passage strictly off-limits to international commercial traffic.

Military analysts suggest that the weekend opening was merely a tactical maneuver, perhaps designed to test Western response times or to allow specific allied vessels a chance to escape the impending lockdown. Regardless of the underlying motive, the resulting whiplash has fundamentally traumatized commodity traders. The unyielding closure reinforces the immense leverage that Middle Eastern geopolitics exert over global energy infrastructure, reminding policymakers from Brussels to Washington that securing maritime trade routes remains one of the most formidable challenges of the modern era.

Mechanics of the Energy Pendulum

The concept of an “energy pendulum” has never been more visible than in the current trading cycles surrounding the Strait of Hormuz. Because nearly one-fifth of global liquefied natural gas (LNG) supplies—largely originating from regional giants like Qatar—must transit through this narrow waterway, any threat of closure introduces immediate scarcity pricing models into the market. As the pendulum swings between hope for diplomatic resolution and fear of a protracted blockade, risk premiums are aggressively attached to forward contracts.

Traders rely heavily on algorithmic forecasting models that instantly process geopolitical developments. When news broke that Iran had slammed the door shut again, automated trading protocols immediately executed massive buy orders for Dutch Title Transfer Facility (TTF) contracts. This herd behavior creates exponential price surges, exacerbating the foundational supply-demand imbalance and forcing European utilities into incredibly defensive hedging positions.

European Natural Gas Futures: A Deep Dive into the Numbers

The raw data from this morning’s trading session paints a stark picture of a market in profound distress. European natural gas futures, which serve as the primary benchmark for continental energy costs, definitively broke through psychological resistance levels. To fully comprehend the sheer magnitude of today’s 11% market jump, one must examine the specific shifts across adjacent commodities and freight indexes.

| Market Indicator | Friday Close | Monday Morning | Percentage Change |

|---|---|---|---|

| Dutch TTF Gas Futures (€/MWh) | €38.74 | €43.00 | +11.0% |

| Brent Crude ($/bbl) | $94.50 | $98.20 | +3.9% |

| LNG Freight Rates ($/day) | $65,000 | $85,000 | +30.7% |

| European Carbon Permits (€/tonne) | €62.10 | €65.40 | +5.3% |

As illustrated in the table above, the shockwave extends far beyond the raw price of natural gas. Freight rates for specialized LNG carriers have exploded by an astounding 30.7%, reflecting extreme vessel shortages as shipowners refuse to deploy assets near the conflict zone without exorbitant hazard premiums. This cascading effect virtually guarantees that downstream energy costs for European manufacturing and residential heating will remain severely elevated for the foreseeable future.

Compounding Pressures from the Ukraine Conflict

The current disaster in the Middle East does not exist in a vacuum; it aggressively compounds the severe vulnerabilities already plaguing Europe due to the ongoing conflict in Ukraine. Since severing reliance on Russian pipeline gas, European nations have pivoted overwhelmingly to seaborne LNG to satisfy their baseload power requirements. By trading one geopolitical dependency for another, the continent has exposed itself to massive maritime supply chain disruptions.

Moreover, the energy infrastructure network is already showing profound signs of strain elsewhere. A concurrent jet fuel crisis in Europe highlights the fragility of regional refining capacities when crude and refined product imports are simultaneously threatened. Industrial output across Germany and Italy is severely threatened, as energy-intensive manufacturing processes simply cannot absorb an extended period of €43/MWh gas without risking massive unprofitability and ensuing widespread factory closures.

U.S. Blockade vs. Iranian Response

The root cause of this morning’s financial earthquake is firmly anchored in the escalating naval confrontation between the United States and Iran. The ongoing U.S. blockade, a highly controversial containment strategy, is intended to severely cripple Iran’s illicit oil export revenues. In response, Tehran has adopted an asymmetrical warfare doctrine, weaponizing its geographic control over the Strait of Hormuz to inflict maximum economic pain on Western allies, particularly those highly dependent on energy imports.

Iran has definitively stated that its territorial waters will remain closed to any vessel perceived as complying with American sanctions or operating under the protection of U.S. naval assets. Consequently, we see headlines confirming the Strait of Hormuz closed again, a narrative that has become agonizingly familiar to global market watchers. The tit-for-tat escalation leaves commercial operators paralyzed, caught between aggressive American compliance enforcers and the very real threat of Iranian military interdiction.

Global Diplomatic and Military Interventions

In a desperate bid to stabilize the global economy, international coalitions are hastily forming to address the crisis. The Hormuz crisis defense mission, spearheaded by European leaders, seeks to provide armed escorts for critical energy cargo. However, military strategists consistently warn that inserting massive flotillas of heavily armed European frigates into the exceedingly narrow confines of the Persian Gulf dramatically increases the risk of a catastrophic miscalculation. Diplomatic backchannels are currently flooded with desperate negotiations, but deeply entrenched political positions in both Washington and Tehran make a near-term de-escalation highly improbable.

What This Means for Global Energy Supply Chains

The ramifications of a sustained closure of the Strait of Hormuz are nothing short of cataclysmic for global energy logistics. Cargo ships that would normally complete a swift transit must now sit idle in safe anchorages, waiting for multi-national escorts, or alternatively face highly complex and expensive rerouting decisions. Because LNG cannot be stored indefinitely without boiling off, these delays result in actual physical losses of the commodity during transit, further tightening the available supply pool upon arrival at European regasification terminals.

Furthermore, marine insurance syndicates based in London and New York have astronomical requirements for war risk premiums. For deeper insight into how broad commodity indexes are reacting globally, you can monitor the Reuters Commodities Index, which consistently details the crippling cost inflation currently battering the shipping sector. Ultimately, these ballooning transit costs are passed directly down to the end consumer, sparking fierce debates among European policymakers regarding massive impending state subsidies to artificially suppress household utility bills.

Evaluating the Risk Premium in Energy Markets

Traders are currently pricing in a severe geopolitical risk premium, an invisible tax layered over the fundamental cost of extraction and liquefaction. Analysts estimate that roughly €12 to €15 of the current €43/MWh price is strictly attributable to the “Hormuz fear factor.” This premium acts as a shock absorber for traders but acts as a wrecking ball for national economies. If the blockade holds firm, we can expect this risk premium to expand exponentially, entirely decoupling regional European gas pricing from global supply-demand fundamentals and entering a realm dictated entirely by political brinkmanship.

Future Projections for TTF Gas Futures

Looking ahead into the third and fourth quarters of the year, the forward curve for TTF gas futures presents a deeply concerning trajectory. While Europe emerged from the previous winter with robust storage inventories, a complete cessation of Qatari LNG imports via Hormuz would fundamentally alter the continent’s refill trajectory. Analysts project that if the strait remains impassable for more than twenty-one consecutive days, European futures could effortlessly breach the €60 per MWh threshold, reigniting the horrific inflationary fires that central banks have spent the last two years desperately trying to extinguish.

Industrial demand destruction will inevitably become the primary market balancing mechanism. High prices will force heavy industries—such as fertilizer producers, glass manufacturers, and steel mills—to shutter operations entirely. This tragic economic reality means that the “solution” to high gas prices will be devastating recessions across major European manufacturing powerhouses.

Navigating the Storm: Policy Alternatives for Europe

Faced with this existential energy threat, European lawmakers are rapidly assessing emergency policy alternatives. A massive acceleration in the deployment of renewable energy infrastructure, specifically offshore wind and utility-scale solar, is currently being fast-tracked through bureaucratic red tape. Additionally, European energy ministries are conducting emergency negotiations with alternative LNG exporters, primarily heavily relying on augmented shipments from the United States and Australia to bridge the impending Middle Eastern deficit.

Yet, these solutions are long-term structural fixes to an immediate, bleeding wound. In the short term, Europe remains totally captivated by the chaotic energy pendulum swinging over the Strait of Hormuz. Until definitive naval de-escalation is secured, or alternative diplomatic frameworks are magically constructed, European markets will remain fiercely volatile, acutely vulnerable, and perpetually reacting to every aggressive maneuver executed in the turbulent waters of the Persian Gulf.

One Comment