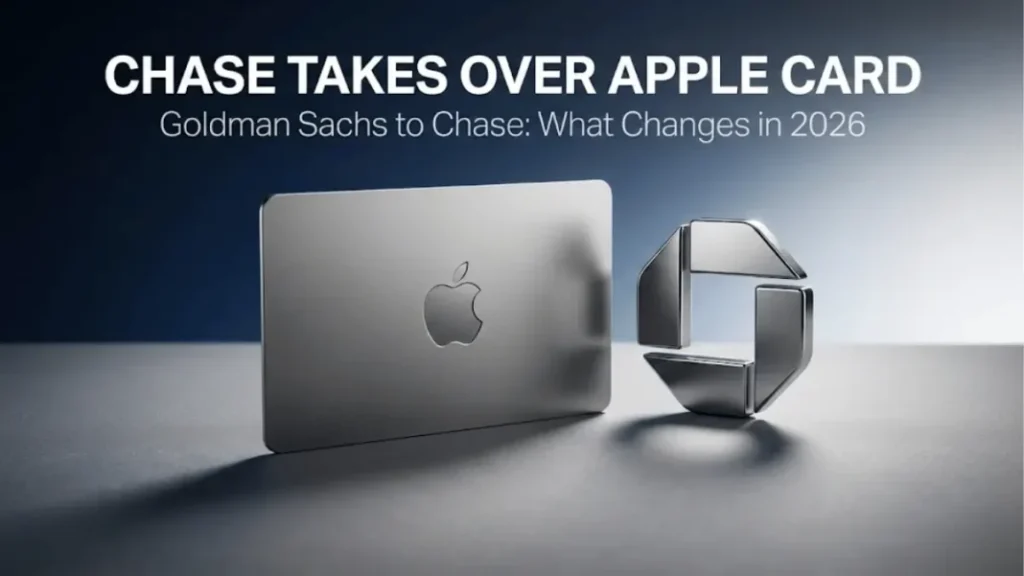

JPMorgan Chase to Become New Apple Card Issuer: Replacing Goldman Sachs in Major 2026-2028 Transition

In a significant development for credit card users and the financial services industry, JPMorgan Chase has agreed to become the new Apple Card issuer, succeeding Goldman Sachs. The deal, announced on January 7, 2026, ends Goldman’s challenging consumer banking venture and positions Chase—already the largest U.S. credit card issuer—as the backbone for one of the most popular co-branded cards.

This JPMorgan Apple Card partnership involves transferring over $20 billion in Apple Card portfolio balances. The Apple Card transition to JPMorgan Chase is expected to take approximately 24 months (potentially completing around early 2028), pending regulatory approvals. Mastercard will continue as the payment network, ensuring continuity for millions of cardholders.

Apple Card users can expect minimal immediate disruption, with all current features—like up to 3% Daily Cash rewards, no fees, and seamless Wallet app integration—remaining intact during the handover.

Background: Why Goldman Sachs Is Exiting the Apple Card Partnership

Launched in 2019, the Apple Card was hailed for its innovative features: no late fees, no foreign transaction fees, Daily Cash rewards, and advanced financial health tools in the iPhone Wallet app. However, the Goldman Sachs Apple Card partnership proved costly for the investment bank.

- Goldman incurred billions in losses from its broader consumer push, with the Apple Card contributing due to higher-than-expected delinquency rates and a portfolio heavy in subprime borrowers.

- Apple’s insistence on broad accessibility led to approving more lower-credit users than typical for premium cards.

- By 2023, Goldman and Apple agreed to wind down the partnership, marking the end of Goldman’s Main Street banking ambitions under CEO David Solomon.

Goldman described the deal as allowing it to “narrow our focus in our consumer business” and refocus on core strengths. The transaction provides Goldman with a positive earnings impact, partially offset by provisions.

Key Details of the JPMorgan Chase Apple Card Deal

JPMorgan replaces Goldman Sachs in a move that strengthens Chase’s dominance in co-branded credit cards (e.g., partnerships with Amazon, United Airlines, and Marriott).

- Portfolio Transfer: Over $20 billion in balances, acquired at a reported discount exceeding $1 billion due to credit risks.

- Financial Provisions: JPMorgan will record a $2.2 billion provision for credit losses in Q4 2025.

- Timeline: Transition expected in about 24 months; no immediate changes for users.

- Savings Account: JPMorgan plans to offer a new high-yield Apple Savings account. Existing Goldman Savings holders can stay or switch.

- Network: Remains on Mastercard.

Jennifer Bailey, Apple’s VP of Apple Pay and Apple Wallet, stated: “Chase shares our commitment to innovation and delivering products and services that enhance consumers’ lives.”

This JPMorgan Chase Apple Card deal highlights Chase’s expertise in scaling large rewards programs while Apple maintains control over the user experience.

Impact on Apple Card Users: What to Expect During the Transition

The Apple Card issuer change prioritizes a smooth experience for cardholders:

- No Immediate Disruptions: Continue earning Daily Cash (up to 3% on Apple purchases, 2% via Apple Pay, 1% elsewhere), using Apple Card Family, and accessing tools like payment trackers.

- Physical Cards: JPMorgan will eventually issue new titanium Apple Cards; details closer to completion.

- Customer Impact: Apple assures seamless service. No action needed now—updates will come via the Wallet app.

- Potential Future Changes: Post-transition, Chase’s stricter underwriting could mean tougher approvals for new applicants. Rewards and core features are expected to stay consistent, as Apple designs the program.

For those concerned about the Apple Card Goldman exit, this switch to a more experienced retail bank like Chase could bring greater stability and potential enhancements.

Future Outlook: Apple Card 2026 Changes and Beyond

As the Apple Card new issuer JPMorgan partnership takes shape, it reinforces Apple’s push into financial services alongside Apple Pay dominance. Chase’s scale could enable innovations in rewards or integrations, while addressing past issues like delinquency rates.

The Apple Card program 2026 and beyond looks promising for users focused on simplicity, privacy, and rewards tied to the Apple ecosystem.

Conclusion

The transition from Goldman Sachs to JPMorgan Chase marks a new chapter for the Apple Card, ensuring long-term stability under one of America’s strongest banks. While the full Chase Apple Card era begins in roughly two years, current holders face little change today. This deal benefits all parties: Apple retains its innovative card, Chase grows its portfolio, and Goldman exits gracefully. Stay informed through official Apple and Chase channels for updates on this evolving JPMorgan Goldman Apple Card story.

Frequently Asked Questions (FAQ)

When will JPMorgan Chase become the Apple Card issuer? The transition is expected to take approximately 24 months, likely completing around early 2028, subject to regulatory approvals.

Will my Apple Card rewards or features change immediately? No. All existing benefits, including Daily Cash rewards, no fees, and Wallet app tools, remain unchanged during the transition.

What happens to my Apple Savings account? JPMorgan will launch a new Apple Savings option. You can choose to switch or keep your existing Goldman Sachs account.

Do I need to apply for a new card? Not yet. JPMorgan will issue new physical cards closer to the transition completion; your current card works as usual.

Will the Apple Card still work on the Mastercard network? Yes, Mastercard remains the payment network with no announced changes.

How does this affect new Apple Card applications? Applications continue as normal for now. Post-transition, Chase’s credit criteria may influence approvals.

Why did Goldman Sachs exit the Apple Card partnership? Due to significant losses, higher delinquency rates, and a strategic shift away from consumer banking.

Is the $20 billion Apple Card portfolio transfer at a discount? Reports indicate yes, over $1 billion, reflecting portfolio risks.